TL;DR: In its first six months, Sunrise brought a fast-growing roster of external assets onto Solana as canonical mints, and together they have traded more than $3.5B onchain across 14M trades and roughly 221K wallets. The newest example is $SPCX, a Backpack Securities-issued tokenized SpaceX product brought onchain via Sunrise the same day SpaceX began trading publicly on Nasdaq. The pattern is clear: getting an external asset tradable on Solana shortly after it lists is becoming the normal case.

Highlights:

- One canonical Solana mint gives wallets, aggregators, and DeFi protocols a shared version to coordinate around from the first hour, instead of starting from fragmented wrapped versions.

- SPCX is one of the sharpest day-one examples: a tokenized public equity reached Solana the same day SpaceX listed on Nasdaq, with $52M across 51 liquidity pools on Solana n the first 24 hours.

- Day-one or early-window tradability is becoming repeatable across different asset types.

- The roster already spans DeFi blue chips, major L1s and L2s, AI and identity tokens, a GPU-backed dollar, an execution network, brand IP, and a sports network token.

Solana Is Where The Trading Already Is

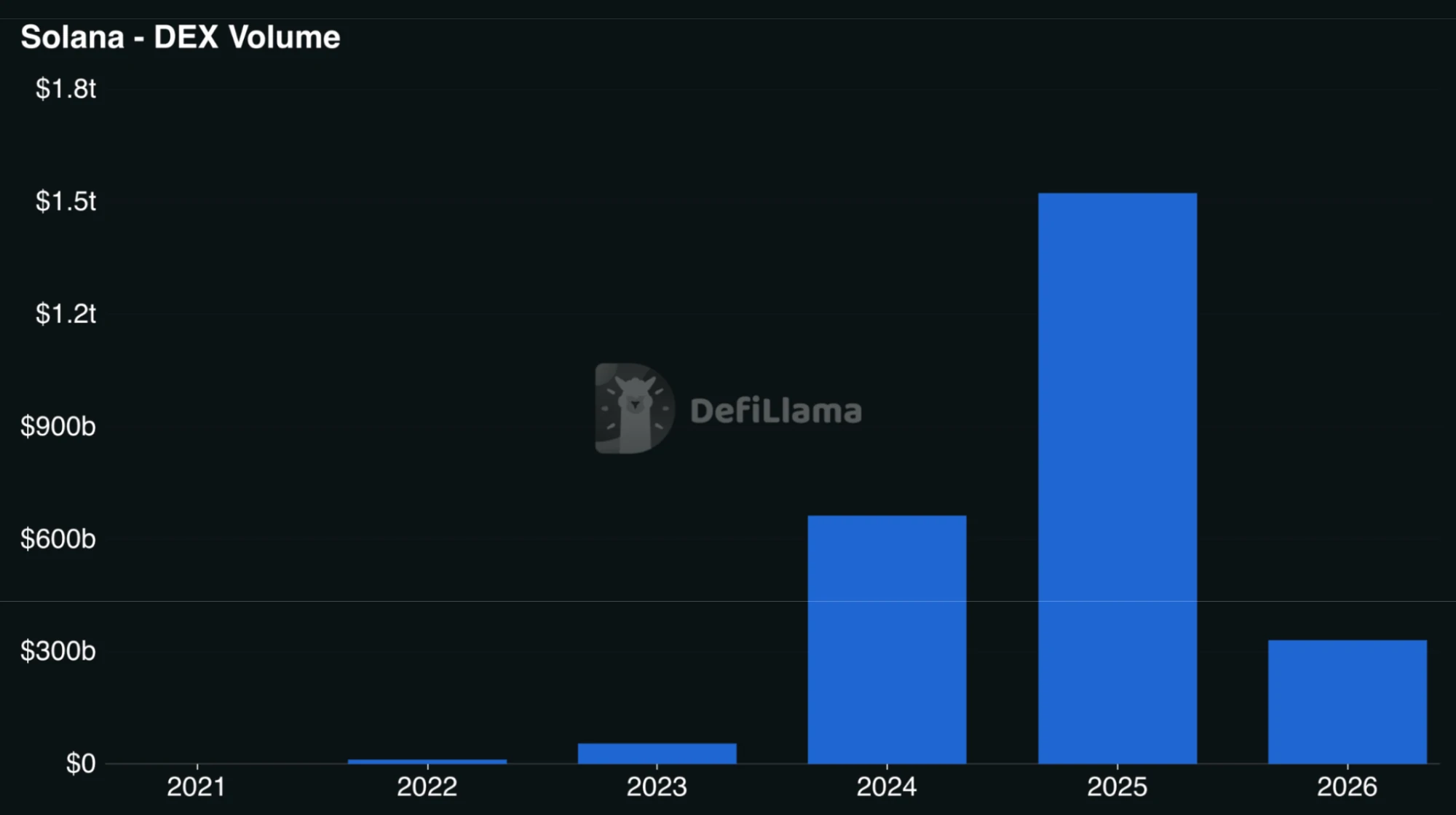

Solana runs one of the deepest onchain trading environments in crypto. Aggregators route across dozens of AMMs, so traders get competitive execution without leaving the network, and deep stablecoin pairs sit underneath all of it. In 2025, Solana processed ~$1.6T in spot DEX volume, one of the largest onchain spot markets in crypto.

External assets do not arrive at an empty venue. They arrive on a network with active traders, deep liquidity, mature routing, and protocols that can move quickly when a new asset reaches Solana in a form they can support. Sunrise is useful because it gives external assets a cleaner way to coordinate around that existing infrastructure from the start. The important distinction is orchestration, not exclusivity. Other representations of an asset may continue to exist on Solana, but the canonical mint gives the market a shared reference point for new liquidity, routing, and integrations.

From Arrival To Liquidity

External assets have long been able to reach Solana through bridge routes. But without a shared canonical path, the same asset can show up through multiple wrapped representations. Sunrise gives the market a single canonical mint to coordinate around instead.

Sunrise uses Wormhole's Native Token Transfers framework to bring an asset into Solana's trading stack as a canonical mint. The result is a single canonical Solana version of the asset that wallets, market makers, aggregators, and lending protocols can point at from day one.

What makes that mint canonical is who controls it. It is the deployment the issuer controls and designates as their official cross-chain version through Wormhole's NTT framework, not a bridge-specific synthetic minted by a third-party custodian. Because the issuer stands behind one address, protocols can commit to it directly: aggregators like Jupiter route to it, and venues like Meteora form pools around it off the same mint.

This does not remove other representations. Wrapped versions of the same asset can still exist on Solana. The canonical mint does not displace them. It gives the market one issuer-designated version to coordinate liquidity and routing around.

That shifts the question from the bridge transaction itself to the market that forms after the asset arrives: where it routes, which pools deepen, which wallets surface it, and which protocols decide to support it.

Three Ways An Asset Has Landed

Six months of listings now sort into three patterns:

- A token that arrived with launch demand already attached

- A tokenized stock product that reached Solana the same day its underlying equity listed publicly

- A token that was already bridgeable and later formed a deeper market

MON: Launch Day, Straight Onto Solana

Monad's token was Sunrise's first listing, on November 24, 2025, the same day Monad's mainnet went live.

Within hours, MON was tradable on Solana's DEX aggregators and AMMs. The first 48 hours on Solana looked like this:

- $131M in volume

- 360K swaps

- 21K unique swapper wallets

Over the first week, Solana processed $213M in MON spot volume, approximately 42% of Monad's own first-week volume.

Six months in, MON has done $374M in total volume across 3.5M trades and 97K wallets. A brand-new token found a live market on Solana from hour one, and it stuck.

SPCX: Public Equity, Onchain On Day One

SPCX extends the Sunrise pattern beyond crypto-native tokens. On June 12, 2026, SpaceX began trading publicly on Nasdaq under the ticker SPCX after the largest IPO in history. The same day, Backpack Securities issued $SPCX as a tokenized SpaceX share, under their regulated securities framework, then used Sunrise to bring it onto Solana as a canonical mint on the same day Nasdaq trading opened.

The important part is market formation, not just the fact that the asset exists onchain. $SPCX did $50M+ in volume across 51 Solana markets in its first 24 hours. And it surpassed $100M in onchain volume in the first 4 days, which spanned over an entire weekend.

A snapshot on Friday, after trading began, showed Nasdaq at $172.86, Hyperliquid perps at $172.62, and Sunrise at $172.82, putting the Solana market close to the Nasdaq reference price.

Source: https://x.com/sunrise/status/2066551052908863711

SPCX is the most direct day-one example yet: a major external asset went public in traditional markets and had a Solana market the same day. The lag between listing, tokenization, and onchain trading compressed into less than an hour.

HYPE: From Bridgeable To Deeply Traded

HYPE shows the difference between presence and market formation. The token had been bridgeable to Solana since Wormhole made it multichain via NTT on September 3, 2025. The Sunrise listing on January 29, 2026 added the routing and pair infrastructure for its Solana market. The roughly five months between "bridgeable" and "deeply traded" is the point: presence is not the same as market formation.

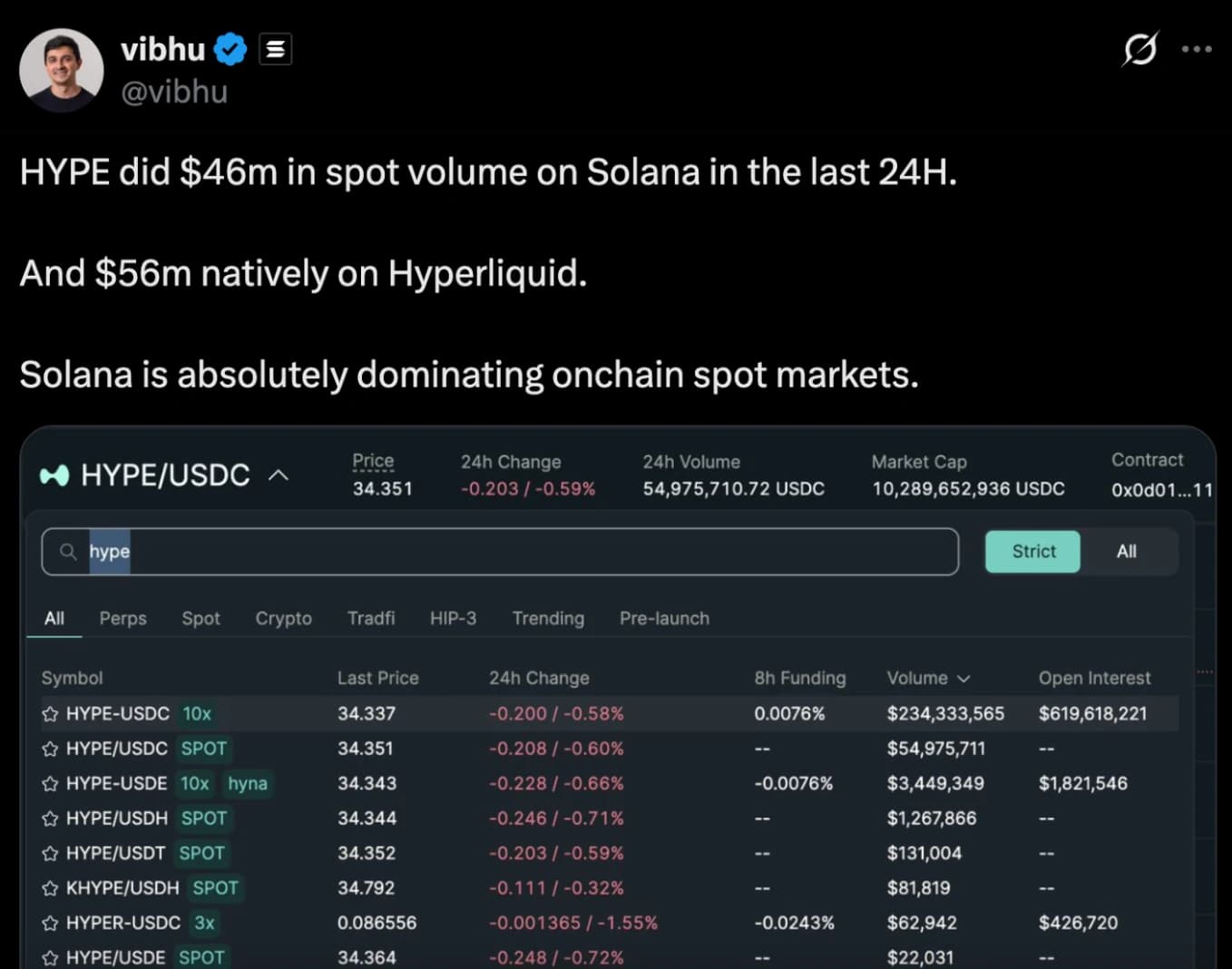

What happened on Solana after the Sunrise listing. In its first seven days, HYPE recorded $102M in Solana spot volume. On March 10, 2026, it ranked fifth by 24-hour DEX spot volume across all Solana tokens, with $46M in Solana spot volume, 7K holders, and $4.58M in onchain liquidity. On the same day, HYPE recorded approximately $56M on its native Hyperliquid L1.

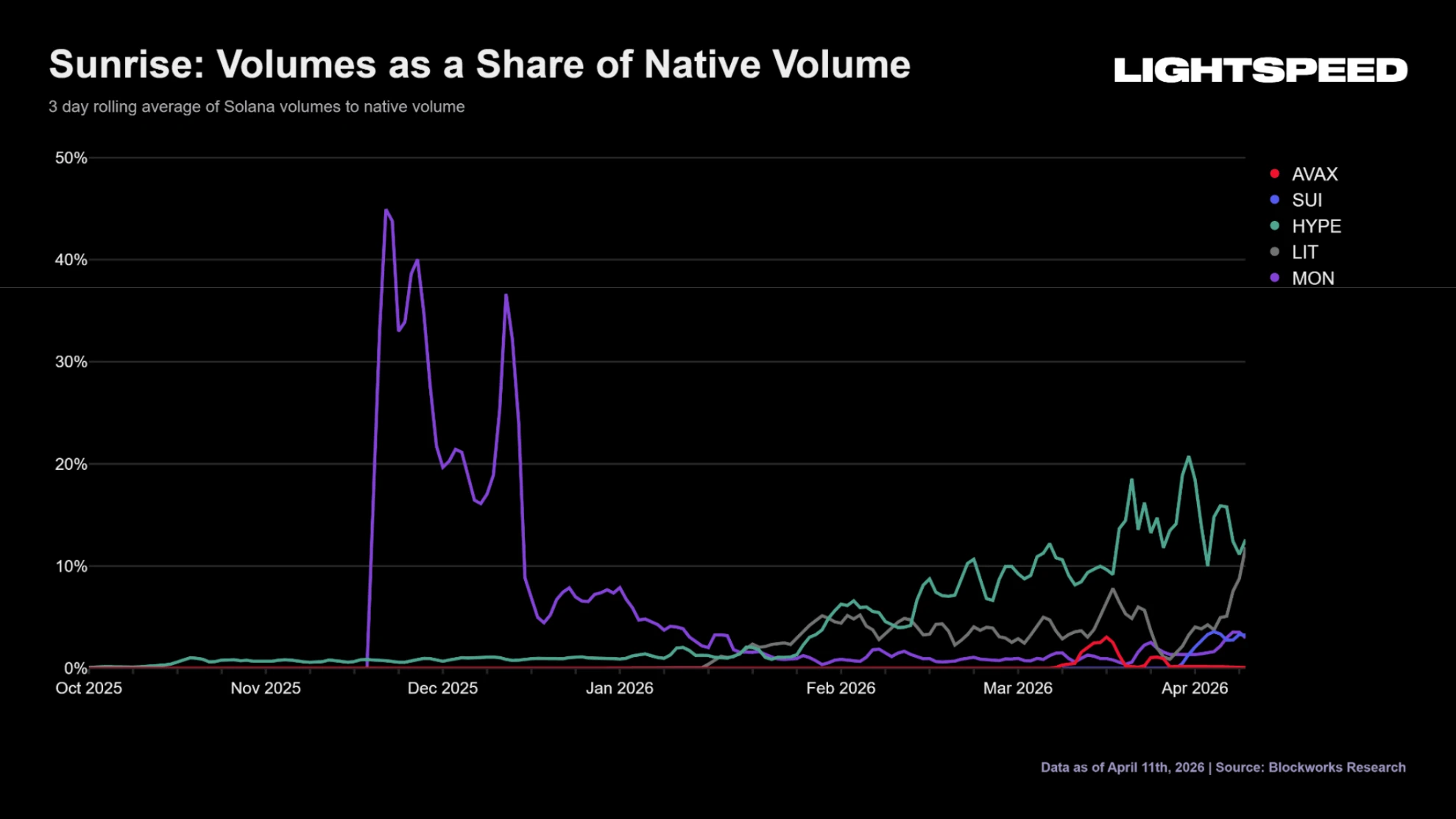

Blockworks Research data through April 11 shows a meaningful and growing share of HYPE's onchain spot activity runs on Solana vs its native chain.

The Long Tail: Many Asset Types, One Canonical Path

MON, SPCX, and HYPE are the headline examples. The broader story underneath is how many different kinds of assets became tradable once their Sunrise market opened. That speed comes from the shape of Solana’s DeFi stack. Aggregators can route new pairs once liquidity exists, wallets can surface the canonical mint, and protocols can evaluate one preferred asset address. The result is not automatic adoption everywhere, but a shorter path from listing to actual use.

The range is the real signal. The roster already includes

- Major DeFi tokens - UNI, AAVE, ENA

- Major L1s and L2s - AVAX, SUI, MEGA

- AI and identity tokens - TAO, and BILL from Billions Network

- GPU-hardware-backed dollar - CHIP from USD.AI

- EVM/SVM/Wasm execution network - BLEND from Fluent

- Brand IP - DMC from DeLorean

- Sports network token - CHZ

- Sports club tokens - PSG, AFC

- Tokenized public equity and ETF - SPCX (SpaceX), MU (Micron), SNDK (Sandisk), DRAM (Roundhill Memory ETF) and BOT (RoboStrategy)

The interesting part is the spread: assets this different all became tradable in the early window after listing.

The roster also includes Backpack’s BP, which is Solana-native rather than external.

What The Numbers Actually Say

Add it up and the first six months come to $3.5B in onchain volume, 14M trades, and about 221K wallets, through mid-June 2026.

Breadth is access, and the canonical-mint path has made that access repeatable: a growing roster of very different assets all reached a live Solana market quickly. Depth is what a market grows into over time, and so far that is mostly HYPE, with MON behind it. This is what early market formation usually looks like. Access can broaden quickly, but volume rarely distributes evenly across every asset. Markets concentrate around the names with the strongest demand, deepest liquidity support, best timing, and most active communities. In that sense, the Sunrise data is less a story about every asset becoming large at once and more a story about many assets getting access to the same arena.

The canonical path can make assets tradable quickly, but it does not decide which ones become deep markets. That comes down to familiar market drivers: real demand, market-maker support, incentives, and how integrated the token gets.

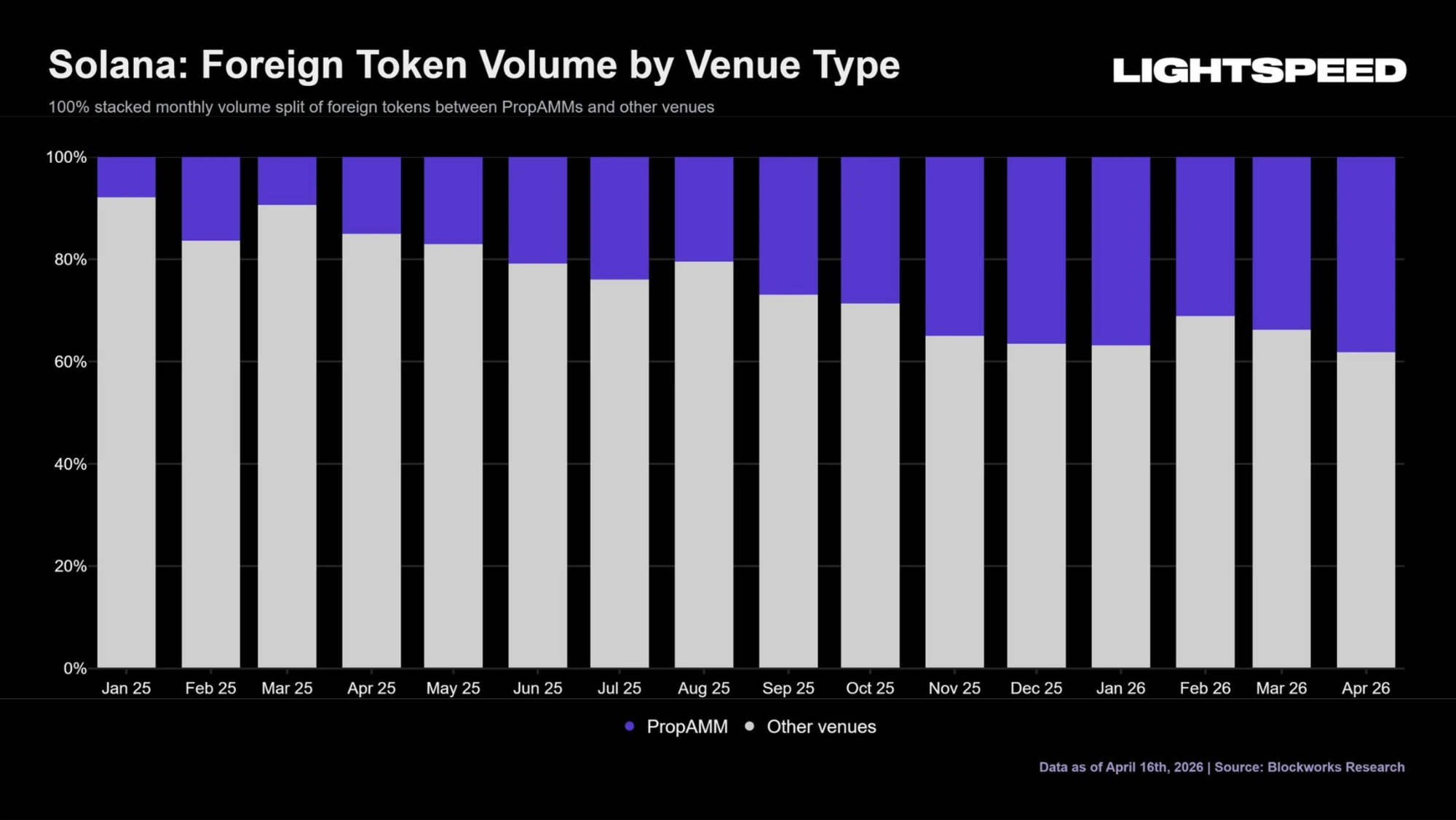

Execution quality is part of that story. Once an external asset has a canonical Solana mint, it can route through the same market structure that supports Solana-native assets. External assets can route through Solana’s broader market structure, including proprietary market-making AMMs where supported. Prop AMMs now handle close to 40% of non-native token volume on Solana, giving external assets access to execution quality comparable to centralized venues. For teams evaluating multichain distribution, Solana offers not only chain expansion, but access to an existing trading stack.

Why Teams Are Showing Up To Solana Earlier

Token markets often form fastest when attention is highest: around launch, major announcements, incentive programs, or new chain expansion. If an asset reaches Solana in a fragmented form, some of that attention goes into figuring out which version to use. If it reaches Solana through a canonical mint, that attention can move directly into swaps, routing, liquidity, and integrations.

That early window does not guarantee a durable market. But it can determine whether the first wave of interest becomes real trading activity or dissipates across venues and token versions. MON is an example of launch attention converting immediately into Solana trading. HYPE is an example of an existing asset developing a larger market once integration caught up with availability.

Teams are showing up earlier because Solana already has the market structure they want to reach. For teams issuing a token or expanding to a new chain, Solana's trading base is the attraction: active traders, deep stablecoin liquidity, mature aggregator routing, and DeFi protocols that move quickly. The practical question is how cleanly a new asset can plug into that environment while attention is high.

For teams, Solana is not only another distribution endpoint. It can become a price-discovery and liquidity-discovery venue. A listing exposes the asset to traders who already live inside Solana’s aggregator and DeFi surfaces, creating a market test that is harder to get from bridge availability alone.

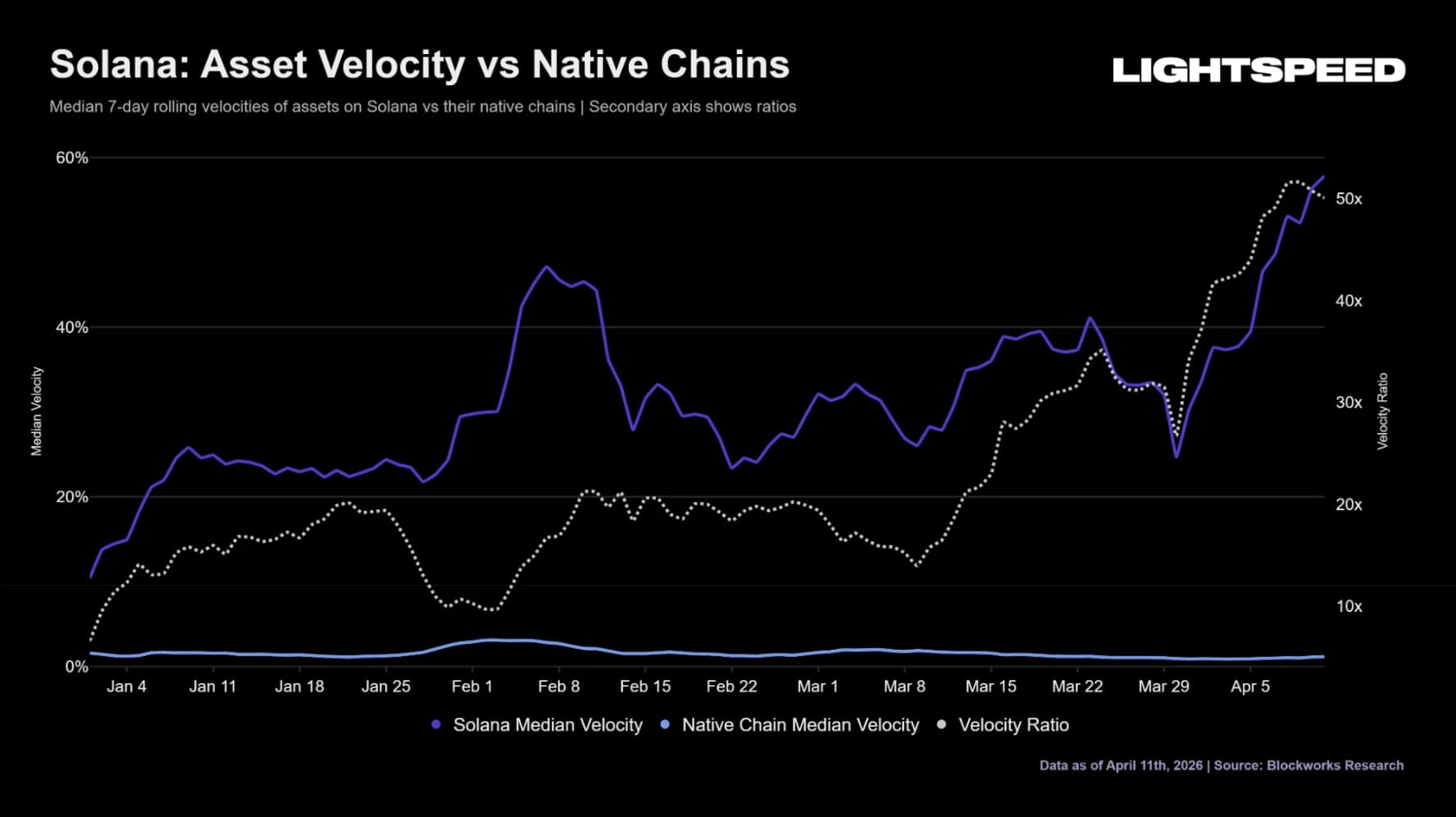

That shows up in velocity. Blockworks Research data through April 11 shows non-native assets generating 20x-50x higher asset velocity versus their origin chains, turning the same unit of available supply into materially more trading activity on Solana. For a team, an early Solana listing buys a live market while the token is still new, on top of the distribution to a new chain.

A canonical mint helps by giving market makers, wallets, and protocols one preferred version and one address to coordinate around. The asset can enter Solana's markets with less ambiguity and a clearer path to liquidity.

What It Adds Up To

Six months of Sunrise data describe a network that can make many categories of external assets tradable quickly when they arrive through a clean canonical path. MON showed launch demand landing directly on Solana. HYPE showed that a token that was merely bridgeable could become one of the network's busiest markets once integrated into routing and trading. The rest of the roster showed that the same path can support a wide range of asset categories.

The broader point is composability. Once an external asset has a canonical Solana mint, it can be routed, traded, displayed, and evaluated by the same infrastructure that already supports Solana-native assets. That is what turns cross-chain distribution from a bridge transaction into a market-formation event.

Internet capital markets are not just about putting assets onchain. They are about making assets usable where liquidity, users, and applications already sit. Sunrise gives one early example of that pattern: assets from outside Solana reaching the network in a form that Solana’s markets can immediately understand.